Key Takeaways

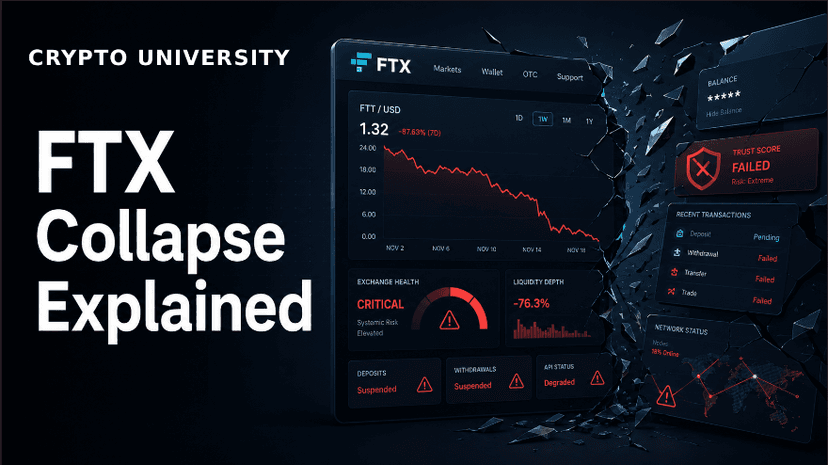

FTX did not fail because of a hack or a market crash. It failed because customer assets sat under company control and were reportedly misused, leaving an estimated 8 billion dollar shortfall when withdrawals surged in November 2022.

The collapse triggered the largest recorded migration from exchange custody to self-custody. Trezor reported sales revenue up roughly 300 percent, Ledger reported new account creation up about 6x, and Bitcoin held on exchanges fell sharply in the following months.

Even though FTX creditors eventually recovered 100 percent or more of their claims, payouts were calculated in US dollars at November 2022 prices. Customers who held Bitcoin missed years of price appreciation, a lesson that legal recovery is not the same as keeping your coins.

Introduction

In November 2022, FTX went from one of the largest cryptocurrency exchanges in the world to bankruptcy in about one week. Millions of customers lost access to their funds overnight. The event is now the most cited case study in crypto education for one reason: it turned an old industry warning, not your keys, not your coins, from a slogan into a documented, measurable market shift.

This case study explains what happened, why custody was the core failure, how user behavior changed afterward, and what the multi-year repayment process teaches about the real cost of trusting a third party with your assets. It is educational content, not financial or legal advice.

What Happened at FTX: A Short Timeline

FTX was founded in 2019 by Sam Bankman-Fried and grew into an exchange once valued at around 32 billion dollars. Its collapse unfolded in days.

Date | Event |

|---|---|

Nov 2, 2022 | CoinDesk publishes a report showing Alameda Research, FTX's sister trading firm, held a balance sheet heavy in FTT, the token issued by FTX itself. |

Nov 6, 2022 | Binance announces it will sell its FTT holdings. Customer withdrawals from FTX accelerate into a bank-run style rush. |

Nov 8, 2022 | FTX halts withdrawals. Binance signs, then abandons, a non-binding rescue deal after due diligence. |

Nov 11, 2022 | FTX files for Chapter 11 bankruptcy. Sam Bankman-Fried resigns. John J. Ray III takes over the estate. |

Nov 2023 | Bankman-Fried is convicted on seven counts of fraud and conspiracy. |

Mar 2024 | Bankman-Fried is sentenced to 25 years in prison. |

Feb 2025 onward | The FTX Recovery Trust begins repaying creditors in phased distributions. |

The Custody Failure at the Center of the Collapse

Strip away the personalities and the headlines and FTX is fundamentally a custody story. When customers deposited crypto or cash on FTX, they gave up direct control. FTX held the private keys and the bank accounts. Customers held an IOU displayed as a balance on a screen.

Court filings and the criminal trial established that customer funds were commingled with Alameda Research and used for trading, venture investments, loans, real estate, and political donations. When users tried to withdraw en masse, the assets were simply not there. The shortfall in customer funds was widely reported at around 8 billion dollars.

Three structural weaknesses made this possible:

Opaque reserves. There was no reliable public proof that customer assets were held one-to-one. Users could not verify anything on-chain.

Self-issued collateral. A large share of the group's claimed assets was FTT, a token FTX created. Its value depended on confidence in FTX itself, so the collateral collapsed at the exact moment it was needed.

No separation between exchange and trading firm. Alameda reportedly had special access to customer deposits, something regulated brokers are legally structured to prevent.

None of these risks were visible in the FTX app. The interface looked the same on the day withdrawals were halted as it did the week before. That is the core educational point: with a custodian, you cannot see the risk until it is too late.

What 'Not Your Keys, Not Your Coins' Actually Means

Crypto assets live on public blockchains, and control of an asset belongs to whoever controls the private key for its address. The phrase not your keys, not your coins summarizes a technical fact, not an opinion:

If you hold the private key (usually backed up as a 12 or 24 word seed phrase), you control the asset directly on-chain. No company approval is needed to move it.

If an exchange holds the key, you own a claim against that company. Your recourse if it fails is a bankruptcy court, not the blockchain.

Before FTX, many users treated this as a purist talking point. Mt. Gox in 2014 had taught the lesson to an earlier generation, but by 2022 exchanges felt professional, well funded, and safe. FTX had celebrity endorsements, stadium naming rights, and a prominent regulatory presence in Washington. Its failure demonstrated that brand strength tells you nothing about custody practices.

The Measurable Shift to Self-Custody

What makes FTX a genuine case study rather than a moral tale is that the behavioral change was measured in real time.

Indicator | Reported change after the collapse | Source of figure |

|---|---|---|

Trezor hardware wallet sales | Sales revenue up roughly 300% week-on-week, higher than during the 2021 bull market peak | Trezor statements to media, Nov 2022 |

Trezor website traffic | Up about 350% over the same period | Trezor statements, Nov 2022 |

Ledger new accounts | New account creation on Ledger Live reported up about 6x | Ledger CEO Pascal Gauthier, Nov 2022 |

Bitcoin held on exchanges | Widely reported drop of roughly 300,000 BTC (from about 2.3M to 2.0M) within about three months | On-chain analytics estimates (Glassnode data as reported) |

Decentralized exchange volume | DEX trading volumes roughly doubled to tripled in the week of the collapse | Dune Analytics figures as reported, Nov 2022 |

These figures are company-reported or analytics estimates rather than audited numbers, but they all point the same direction. Exchange outflows approached record levels in mid-November 2022 as users moved coins to wallets they controlled. Analysts have described it as the largest migration from exchange custody to self-custody in crypto history.

How the Industry Changed After FTX

Proof of reserves became an expectation

Within weeks of the collapse, major exchanges including Binance, Kraken, and OKX published or expanded proof-of-reserves reports, often using Merkle tree techniques that let individual users verify their balance is included in the exchange's attested holdings. Proof of reserves has real limitations, since it shows assets at a point in time and does not always prove liabilities, but the norm shifted from trust us to show us.

Regulators moved faster

FTX became a reference point in policy debates worldwide. The European Union finalized its MiCA framework, which includes custody and segregation requirements for exchanges. In the United States, the collapse shaped years of enforcement actions and legislative proposals focused on separating customer assets from company assets. This article does not offer legal advice, but the direction is clear: segregation of customer funds became a central regulatory theme.

Custody itself became a product category

Institutional adoption after 2023, including spot Bitcoin ETFs, was built on regulated, insured, segregated custodians rather than exchange accounts. At the retail level, wallet technology improved, with cheaper hardware devices, multi-signature setups, collaborative custody services, and smart contract wallets with social recovery reducing the risk of a single lost seed phrase.

The Repayment Lesson: Recovered Is Not Made Whole

The FTX bankruptcy produced a surprising outcome. Through asset recovery, lawsuits, and the rising value of estate holdings, the FTX Recovery Trust assembled well over 15 billion dollars and began repaying creditors in 2025. By early 2026, roughly 10 billion dollars had been distributed, and smaller convenience class claims reached a cumulative recovery of about 120 percent of their claim value.

Distribution round | Approximate date | Approximate amount |

|---|---|---|

First (Convenience Class, claims under 50,000 dollars) | February 2025 | 1.2 billion dollars |

Second (larger claim classes) | May 2025 | 5 billion dollars |

Third | September 2025 | 1.6 billion dollars |

Fourth | March 2026 | 2.2 billion dollars |

Further rounds | Scheduled into 2026 and 2027 | Ongoing |

On paper, 120 percent sounds like customers came out ahead. The catch is that claims were valued in US dollars as of the bankruptcy petition date, November 11, 2022, when Bitcoin traded near 17,000 dollars. A customer who held 1 BTC on FTX received a claim worth about 17,000 dollars, plus interest, paid out years later in dollars. That same Bitcoin was worth several times more by the time payments arrived. Self-custodied holders kept their coins and their upside. FTX customers received a dollar refund on a snapshot from the worst week of the bear market.

This is the most underrated lesson of the case. Even in a best-case bankruptcy with historically high recoveries, custodial failure cost customers years of time, extensive KYC and tax paperwork, and the entire price appreciation of the assets they thought they owned.

The Honest Trade-Offs of Self-Custody

Responsible education means acknowledging that self-custody transfers risk rather than eliminating it. You remove counterparty risk and take on personal operational risk.

Factor | Custodial (exchange holds keys) | Self-custody (you hold keys) |

|---|---|---|

Counterparty risk | High. You depend on the company's solvency and honesty | None for storage. No company can freeze or lose your coins |

User error risk | Low. Password resets and support exist | High. A lost seed phrase or a signed malicious transaction is usually unrecoverable |

Phishing and scam exposure | Account-level attacks | Wallet drainers, fake apps, and seed phrase theft target self-custody users directly |

Convenience | High. Easy trading, recovery, and fiat access | Lower. You manage backups, devices, and transaction verification |

Verifiability | Limited. Depends on disclosures like proof of reserves | Full. Balances are verifiable on-chain at any time |

Inheritance and estate planning | Handled through the company's legal process | Your responsibility. Requires deliberate planning |

A common practical pattern that emerged after FTX is a hybrid approach: keep only active trading funds on reputable exchanges, and move long-term holdings to a hardware wallet or multi-signature setup. This is a risk-management pattern users adopt, not a recommendation for any individual situation.

Practical Lessons from the FTX Case

For learners who want to act on the case study, these are the widely taught starting points:

Understand what you actually hold. An exchange balance is a claim on a company. Coins in a wallet you control are on-chain assets. Know which one you have.

Learn self-custody with small amounts first. Set up a reputable hardware or software wallet, send a small test transaction, and practice restoring from your seed phrase before moving meaningful value.

Protect the seed phrase offline. Never type it into a website, never photograph it, never share it. Anyone with those words controls the funds.

Evaluate custodians critically. Look for proof of reserves, regulatory status, segregation of customer assets, and transparent corporate structure. Marketing and sponsorships are not evidence of safety.

Diversify custody risk. Avoid concentrating everything in a single exchange, a single device, or a single backup location.

Conclusion

FTX changed self-custody forever because it converted a philosophical argument into hard data. Before November 2022, holding your own keys was often framed as an ideological preference. Afterward, the numbers spoke: hundreds of thousands of Bitcoin left exchanges, hardware wallet makers sold out of stock, proof of reserves became an industry standard, and regulators wrote custody segregation into law. Even the remarkable creditor recoveries reinforced the point, because getting dollars back in 2026 at 2022 prices is not the same as never losing control of your coins. The most durable lesson is simple to state and worth teaching to every new market participant: verify what you can, control what you can, and never confuse a balance on a screen with an asset you actually hold.

FAQ

What caused the FTX collapse?

FTX halted withdrawals in November 2022 after revelations about its sister firm Alameda Research triggered a run on deposits. Customer funds had been commingled and used by Alameda, leaving an estimated 8 billion dollar shortfall. The company filed for bankruptcy on November 11, 2022, and founder Sam Bankman-Fried was later convicted of fraud and sentenced to 25 years in prison.

What does 'not your keys, not your coins' mean?

It means that whoever controls a private key controls the crypto at that address. If an exchange holds the keys, you hold a claim against the exchange rather than the asset itself. If the exchange fails, your recourse is bankruptcy court.

Did FTX customers get their money back?

Largely yes, in dollar terms. The FTX Recovery Trust began phased distributions in February 2025, and by 2026 many claim classes reached 100 percent recovery or more, with smaller claims reaching about 120 percent. However, claims were valued at November 2022 prices, so customers who held crypto missed the subsequent price appreciation.

Is self-custody safer than keeping crypto on an exchange?

It removes counterparty risk but adds personal responsibility. Self-custody protects you from an exchange failure, while exposing you to risks like losing a seed phrase or signing a malicious transaction. Many users manage this by keeping only active funds on exchanges and long-term holdings in wallets they control.

What is proof of reserves?

Proof of reserves is a disclosure method, often using Merkle trees, that lets an exchange demonstrate it holds assets matching customer balances, and lets individual users verify their account is included. It became a widespread industry practice after the FTX collapse, though it has limits because it does not always prove liabilities or off-chain obligations.

Disclaimer: This content is for educational and informational purposes only and is not financial advice. Nothing here is a recommendation to buy or sell any asset or use any platform. Do your own research and manage your risk.

What Is a Liquidity Pool? How AMMs Replace Order Books